The war in Iran has brought an urgency to securing domestic supply of raw materials including plastic resin. And parts of the struggling recycling sector are seeing upside in sharp rises for commodity pricing. Read on to learn more about pricing drivers for some of the most common types of plastics bales.

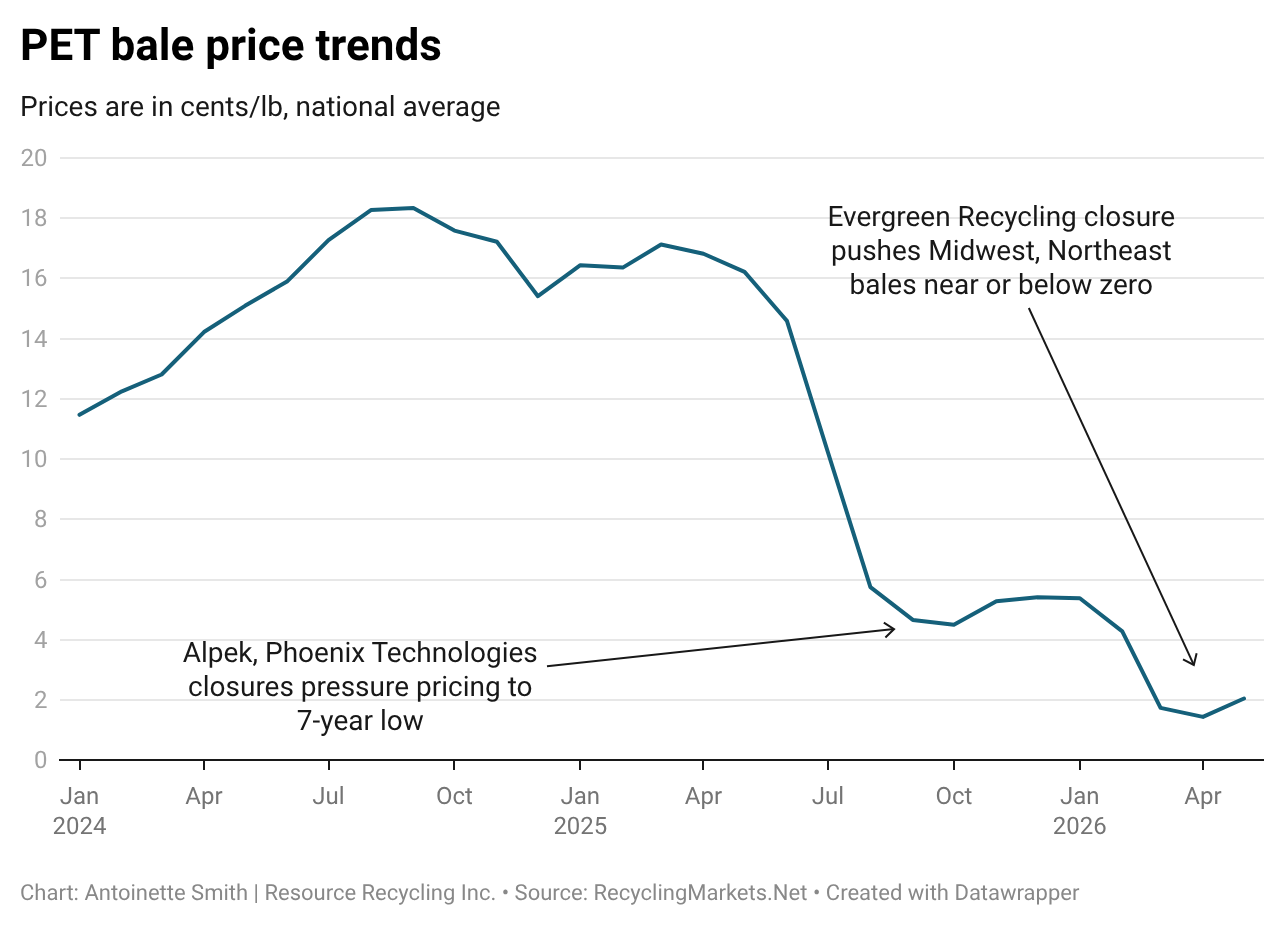

PET

If anyone needed evidence that PET bales are hyper-regional, this spring has provided it. California fundamentals are always disconnected from markets east of the Rockies, but now pricing is showing a stark spread between northern and southern regions.

Bale prices in the south and southeast are around 5 cents/lb but the Upper Midwest/northeast prices are in the very low single digits. The Upper Midwest is far from the biggest converters, and high diesel prices have limited purchasing to local suppliers, whose higher bale prices may be offset by lower freight costs. However, trucking rates were heard easing late in the week ended May 10, possibly due to reduced demand.

In addition to distance from buyers, Northeast recycling systems were particularly hard hit by recent plant closures, plus the region has a concentration of deposit return systems that provide steady supply.

There are plenty of bales out there, but converters in the Southeast are getting what they need without paying exorbitant freight prices, while bales are stacking up in more distant regions.

Looking ahead, US buyer appetite for imports could diminish. Imported volumes are inherently risky even in normal circumstances, without the added uncertainty related to the Strait of Hormuz closure. And virgin PET pricing typically correlates with crude oil movements, because more than half of its makeup is crude-derived.

Some estimates say recovery will take nine months to a year – from the time war is actually resolved.

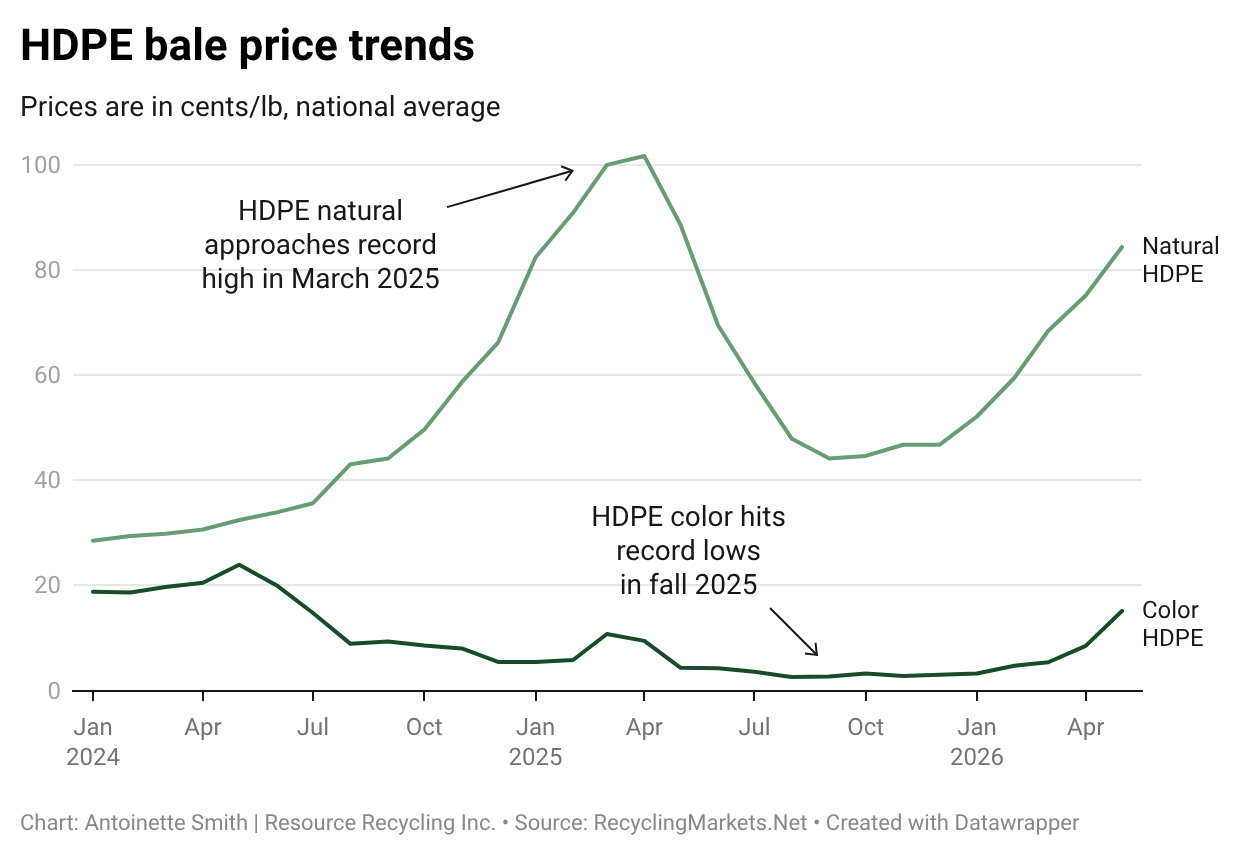

HDPE

Natural bales are skyrocketing once again, as they like to do after a crash every other year or so. Color bales are also ticking up, though the spread with natural has remained wide for the past 18 months. The February storm that gripped at least one-third of the US hindered collection, and tightened supply for weeks as a result, but seasonality is picking up, to the extent that natural HDPE markets reflect this.

Color bales are largely used in construction applications, such as pipes, and that sector has been subdued for most of the past three years. In addition, Q1 exports of PE scrap were down by 15% on the year, at 28,752 mt, according to US International Trade Commission data. In the absence of domestic demand for color HDPE, bales may be exported especially to Southeast Asia.

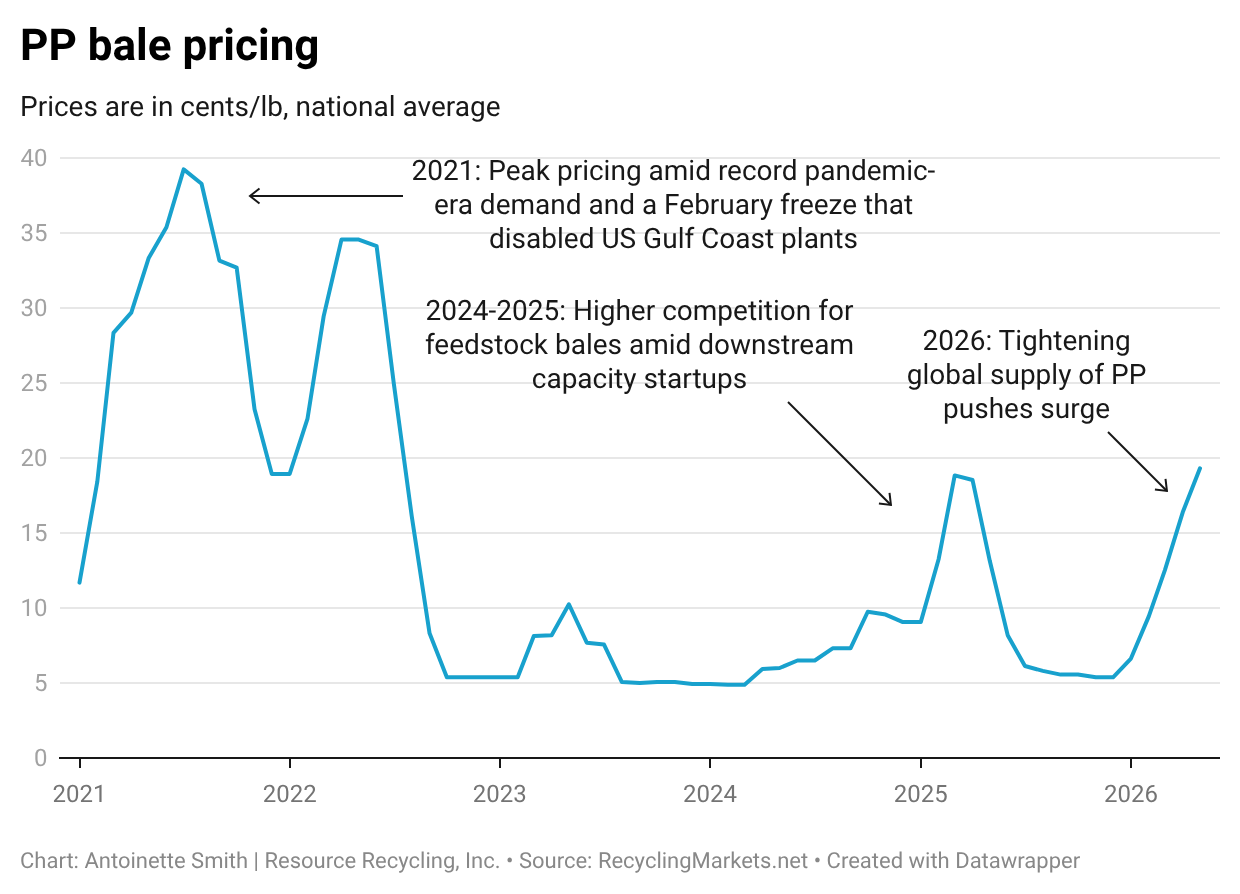

PP

And finally, PP bales are having a moment – again. Prices were steady for nearly two years, before surging as two large buyers stocked up ahead of capacity additions, then dropped for H2 2025, and now are surging again.

In a Q1 earnings call May 7, Republic Services said war-related feedstock constraints in other regions are supporting wider resin price spreads for the company’s polymer centers as well as the Blue Polymers polyolefins production JV with Ravago. And during the quarter, production volumes increased across the polymer center network.