With the war in Iran in its fourth month, pricing for virgin plastics has skyrocketed, but in the longer term, weak overall demand will outweigh temporary factors, according to an ICIS recycling analyst.

Pricing for recycled polymers is reacting to “pretty aggressive” price spikes in virgin resin, rather than to an uptick in demand, said Andrea Bassetti, Americas team lead for recycling at the commodity analytics company.

And even large events like the World Cup will do little to spur demand. “In a normal market, that would have had an impact, but at the moment, that’s kind of out of sight, out of mind,” Bassetti said. “The impact of the conflict is way bigger than anything else. It’s going to continue outweighing any smaller dynamic.”

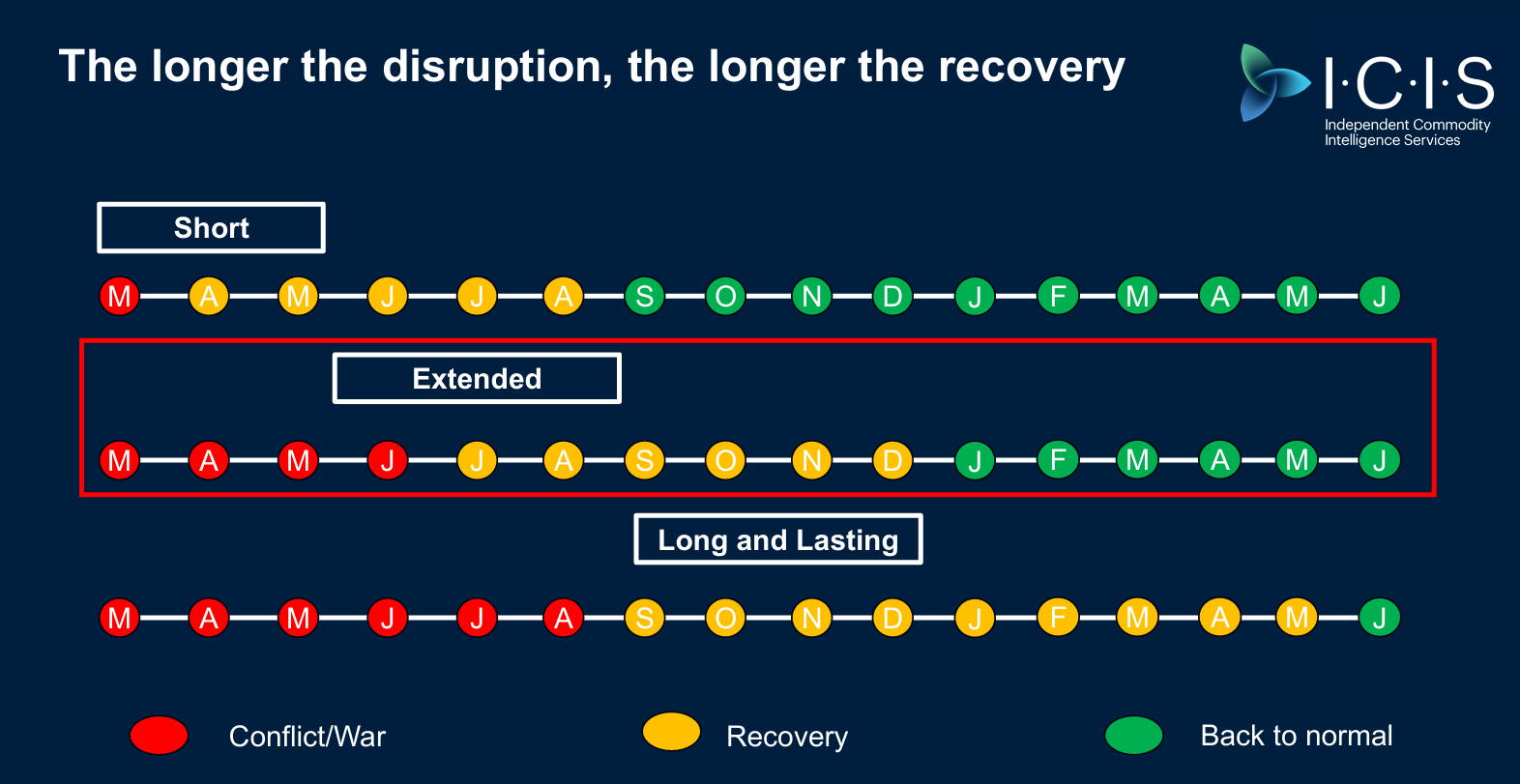

Already the war has gone on long enough to extend the length of recovery too, she said, adding that under the current scenario, recovery would last through the end of 2026. “But if the conflict continues longer, then that recovery period is also way longer.”

For example, if no resolution emerges before September, the length of recovery would extend from about six months to nine, according to ICIS modeling.

ICIS models consider the conflict to be in the “extended” scenario, having already surpassed the “short” timeline. | Graphic courtesy of ICIS

Recycled, prime markets recouple

After a period of decoupling from virgin resin, pricing for all recycled plastics is highly correlated again, she said.

“There’s been a reset button pressed on all the polymers, and they’re all extremely correlated to what’s going on in virgin,” she said. “All the virgin counterparts have increased a little bit more aggressively than the recycled counterparts, but it’s gotten to the point where as soon as there’s a price increase on the virgin side, you’ll see it on the recycled side as well,” especially for flake and pellet.

However, so far prices for recycled plastics are largely notional, she said, not as a result of an increase in transactions. “We haven’t necessarily seen usage of recycled material increase that drastically, and it’s tough to say why,” she said.

Historically when virgin plastic prices are at parity with or higher than recycled resin, end users have substituted recycled material wherever possible. But now, “we haven’t necessarily seen that. Nobody’s willing to take any risks.”

She added that given how weak demand is, ICIS does not expect to see increased adoption, unless the elevated virgin PET prices are sustained.

Bassetti also noted that adopting recycled content into existing production processes is gradual, even if the end user has already qualified the material. Making the switch would affect their supply chains for several months, with no certainty as to what future pricing will look like, Bassetti said.

In PET bale markets, pricing has diverged, depending on the polymer and grade, she said. Pricing for East Coast curbside PET bales has remained flat even as flake and pellet prices tracked rises in virgin markets, as a result of the concentration of PET closures in the region and the resulting buildup of bale supply.

Europe has started to pick up some of the excess bales, particularly Turkey and Germany, she added.

The West Coast, however, is experiencing an entirely different dynamic. The demand pull from Mexico is helping to support bale pricing in that region, as US bales are significantly less expensive than in Mexico. “That might be one of the only dynamics at the moment, demand-wise, that doesn’t really have to do anything with the Iran conflict.”

And until there is some resolution to the Iran conflict, ICIS forecasts for recycled resin prices will follow the outlook for virgin resin, Bassetti said, and toward the end of the year, she expects RPET premiums to normalize to 20% to 30% higher than virgin.

Seasonal patterns ‘out the window’

For RPET, summer typically is the high season, with bale pricing rising with increased demand starting around early March as the bottling supply chain ramps up production for the peak summer beverage season. July 4 is the traditional peak for summer demand, after which post-consumer bottle supply starts to become abundant once more.

But “with everything that’s happened, that demand pattern has been thrown out the window, and we’ve made it past the point where we would have seen that demand for beverage season, for thermoforms, and so we’re going to start entering a period where supply is going to be even longer, because it’s hot, summer starts, and everybody’s buying again.” She added that HDPE grades and polypropylene would likely see slightly different patterns.

For the longer term, demand from Latin America will grow in the medium to long term, amid investments from Arca Continental and other factors, she said. Already additional demand for RPET has come from Colombia and Mexico.

ICIS also believes that demand is coming from Brazil, which is using trade policy to protect its burgeoning domestic RPET industry, imposing stiffer import taxes to discourage plastic scrap imports while also implementing minimum recycled content laws. “I think the demand pull is only going to increase over time.”