This article originally appeared in the Summer 2018 issue of Plastics Recycling Update. Subscribe today for access to all print content.

Thus far in 2018, North American recycling companies have encountered plenty of headwinds when it comes to international trade, with processors, brokers and others trying to determine what to expect next on import policies in Asian markets.

But just as the industry was starting to adjust to the realities of National Sword, another globally oriented issue brought complications to recycling: the multi-billion dollar tariff battle being waged between the U.S. and longtime partners, most notably China.

The duties have directly impacted the steel and aluminum markets, leading to boosted prices garnered by metals processors.

But far more recycling stakeholders stand to be affected through higher costs for equipment, vehicles and other important day-to-day items made of metal. In addition, questions linger in terms of impacts on the wider plastics market, material choices by product and packaging makers, and the health of the U.S. economy as a whole.

“Certainly, I think the potential implications of the trade war have reverberated around markets everywhere, whether it’s commodities markets, stock markets or currency markets,” said Joe Pickard, chief economist of the Institute of Scrap Recycling Industries (ISRI). “We’ve had an extended period of economic growth, and this is one of the things that could really derail that.”

Below, we’ll outline the ways this global economic issue is already shifting recycling realities, and we’ll analyze some of the longer-term impacts and unknowns a sustained international trade war could bring to materials recovery stakeholders.

Feeling shift in multiple ways

It’s true the tariff situation is multifaceted and evolving day by day (or tweet by tweet), making it a hard issue to succinctly characterize. But for Joe Jurden of Cook Paper Recycling Corporation in Kansas, one of the most pronounced impacts on his company is simple to describe.

“Something everyone in the recycling industry is feeling right now is the effect on baling wire,” Jurden said, noting that in the wake of steel tariffs, the cost of that materials-recovery staple has risen 10 to 12 percent. “Most budgets don’t have that kind of leeway. And it’s not over.”

The price of baling wire encapsulates what’s occurred in the steel market since President Donald Trump in March announced his administration would impose tariffs on steel and aluminum imported into the U.S. The tariffs, levied at 25 percent on steel and 10 percent on aluminum, took effect March 23. Soon after the U.S. duties were in place, China hit back with tariffs of its own, including a 25 percent tariff on scrap aluminum.

Since June 1, the U.S. steel tariffs have been extended to imports from all countries except Argentina, Australia, Brazil and South Korea, and the aluminum tariffs on all countries other than Argentina and Australia.

That activity has sent metals markets into a tizzy. The benchmark pricing for U.S. steel climbed roughly 40 percent over the first seven months of 2018, hitting a 10-year high in June. Aluminum values, meanwhile, hit a seven-year high in April, but fell from there, in large part due to U.S. sanctions on a major Russian manufacturer.

Recycling companies are experiencing the early fallout from these market shifts in multiple ways, some good and some bad.

Take, for example, Chicago-area Lakeshore Recycling Systems. The company handles residential and commercial recyclables, including construction and demolition debris.

Alan Handley, Lakeshore’s CEO, said the price of scrap metal went through the roof when the steel and aluminum tariffs were announced. That has boosted revenues for Lakeshore’s sorting facilities that handle significant tonnages of scrap metal.

But tariffs have caused problems for Lakeshore in other ways.

Hardest hit have been the steel containers Lakeshore purchases to provide to commercial customers. Handley said the price of a 30-yard roll-off box has increased by about 20 percent since tariffs went into effect.

More problematic than price, however, is the lack of availability. “Wait times have dramatically increased, if you can even get them,” he said.

In the wake of steel tariffs implemented this spring, the cost of baling wire increased 10-12 percent. “Most budgets don’t have that kind of leeway,” said one processing executive.

Handley noted that costs for packer trucks have also increased, and although the boost hasn’t been huge, if the market doesn’t equalize over time, the increase will have an impact.

“[The Chicago area is] a big market, and there’s a lot of people using steel for other stuff,” he said. “So the ability to get steel is just much more difficult than it used to be.”

Another tariff impact is less about the products covered by additional duties, and more about the process by which tariffs are being implemented. Tariffs were proposed, then halted, then brought back again, and that kind of uncertainty creates an unstable business climate, according to company leaders.

“Things are on and things are off very quickly,” Jurden said.

Woes for equipment manufacturers

Recycling equipment makers say they have seen similar impacts in terms of costs and wait times for the metals that are essential to their offerings. That fact is almost certainly going to mean higher prices for those operators who make machinery purchases in the coming months and years.

“In manufacturing, we’re in a high-overhead position,” said Ashley Davis, director of sales and marketing at CP Group. “Any direct cost we incur we have to pass on. Nobody likes it, but it is what it is.”

According to Davis and Mike Whitney, CP Group’s vice president of operations, the company started to see considerably higher steel prices at the end of last year – the economy was growing and so was demand for the metal. When tariffs were introduced in early 2018, the price jumped a little more, by roughly 20 percent, but the main factor continued to be market demand, according to the CP Group executives.

According to Davis and Mike Whitney, CP Group’s vice president of operations, the company started to see considerably higher steel prices at the end of last year – the economy was growing and so was demand for the metal. When tariffs were introduced in early 2018, the price jumped a little more, by roughly 20 percent, but the main factor continued to be market demand, according to the CP Group executives.

Whitney said the company in July of this year was paying significantly more for steel than it was last summer. He noted CP Group uses a few million pounds of steel annually – predominantly from steel mills in the U.S. and South Korea – and steel expenses account for 20 percent to half of the cost of a typical buildout of a new recycling facility or retrofit.

Similar to what Handley from Lakeshore has experienced, delivery times have also been an issue for CP Group.

Whitney gave the example of tube steel, which is used to make the walls of bunkers in recycling facilities. In June, CP Group’s warehouse got down to its minimum level of the material. “We placed an order with one of our steel suppliers,” Whitney said. “Generally, we’ll get it in a couple of days. This time it took us three weeks.”

Chris Hawn, CEO of Machinex Technologies, said input costs have gone up considerably for his company as well. Though Quebec-based Machinex does all its manufacturing in Canada and is therefore not directly affected by tariffs on steel imported to the U.S., the company still must deal with the boosted price of steel on the commodities market.

Hawn said no customer likes the idea of having to pay more for goods, but he added recycling companies have been understanding thus far, grasping the fact that higher equipment prices are due to larger forces.

“It’s not just equipment,” Hawn said. “There’s going to be increases in the price of automobiles and all other types of steel goods. We’re not the only industry being hit.”

But higher equipment costs do have an extra sting right now, thanks to the other global phenomenon unfolding in the recycling world. The import reductions and new contamination specs enacted by China and other Asian nations have forced domestic processors to scramble to produce cleaner bales. For many companies, part of the strategy has been integrating more equipment.

“Last year and this year were two of our busiest years in terms of sales,” said Davis of CP Group. “We have been really heavy on retrofits, cleaning up fibers and optical sorters.”

With Asian customs authorities indicating more import restrictions could be on the way and domestic buyers continuing to call for higher-quality bales, the push for more help on the sortation front seems set to continue. The fact that tariffs could make such efforts more difficult is not what stakeholders want to hear.

“Anything that could increase the costs for updating plants and the plastics recycling infrastructure would be of significant concern,” said Steve Alexander, executive director of the Association of Plastic Recyclers. “Anything that increases the price of equipment would be the wrong thing to do.”

What potential plastics tariffs mean

While the tariffs that have been enacted thus far have produced recycling ripples mainly in terms of the steel market, the longer-term effect could spread wider.

One key question is whether more rounds of duties will be implemented by the Trump Administration. The U.S. in early July enacted 25 percent tariffs on $34 billion worth of Chinese imports after a U.S. investigation alleged unfair trade practices on China’s part. Those tariffs cover various machinery components and other products “containing industrially significant technologies,” according to the Office of the U.S. Trade Representative, which is part of part of the Trump cabinet.

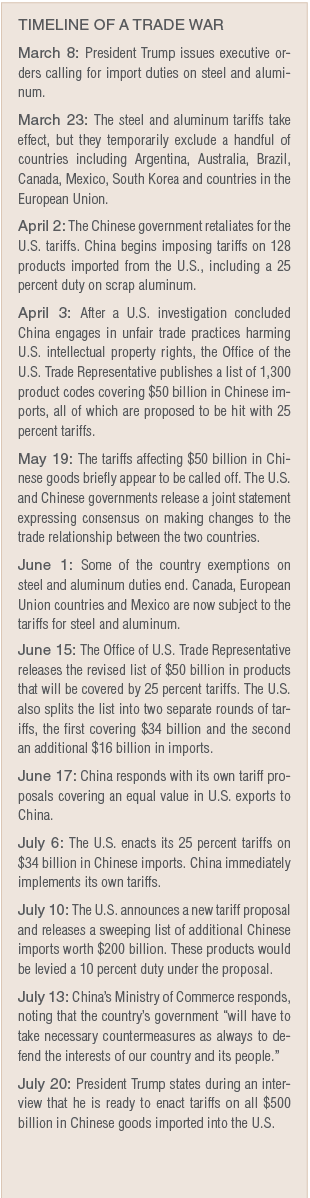

China immediately responded by enacting tariffs of equal value on a variety of U.S. products. Since that tit-for-tat, tariffs affecting billions of dollars worth of additional trade have been discussed, and China and others have noted they are set to continue retaliating. (See the timeline on page 30 for a full rundown.)

An area of note for the recycling industry is the possibility of duties on the virgin plastics and chemical industry. Beyond the tariffs that have already been implemented, in successive retaliatory threats, the U.S. and China have each proposed tariffs on an additional $16 billion in imports from the other country. Those lists both include virgin plastic resins. And the U.S. has proposed yet another list covering $200 billion in imports, which includes numerous plastic materials and elicited yet another vow of retaliation from China.

The possible effects on prime plastics have relevance to the recycling industry because recycled resin prices tend to follow their virgin counterparts.

The Chinese government’s proposed $16 billion list includes LDPE, LLDPE and some non-commodity grade PE resins.

But according to Kailin Fu, associate director of polyolefins and engineering plastics for IHS Markit Chemical, the immediate impacts on U.S. resin markets if such levies did go into effect would likely be relatively minimal.

For example, she noted the U.S. sends a little less than 1 million metric tons of PE to China each year, which is 17 percent of total U.S. PE exports. Of the PE entering China, only 14 percent is covered by the tariffs.

On the U.S. side, the list of proposed tariffs covering $16 billion in imports from China includes many PE and PP resins, as well as some finished goods.

The list “basically covers all the PE family,” Fu explained. But that doesn’t mean a massive impact: In 2017, Chinese shipments to the U.S. only accounted for about 2 percent of the U.S. PE demand.

But it’s a different story for finished goods, which are a major export from China to the U.S. The $16 billion tariff list covers pipe, film and sheen, and the additional $200 billion list includes PE bags and sacks.

The possibility of tariffs on plastic resin shipments could dissuade investment in the U.S. by companies looking to produce recycled-content pellet that they would export to China.

“That’s 90 percent of all the finished goods we track,” Fu said.

If huge quantities of these goods could no longer be moved into the U.S. market, the reverberations through global manufacturing chains, including material demand, could be significant.

Still, Fu said it’s too early to sound serious alarm bells on the issue. “Right now, we really don’t expect prices to go drastically high or low on either side,” she said. “The pricing factor for recycled really isn’t obvious yet.”

One pricing component that could prove relevant to the recycling industry is the impact on the growing number of operations looking to ship recycled resin to China.

Since China enacted major restrictions on scrap plastic imports, many Chinese plastics recycling companies have set up new facilities outside the country. They receive raw scrap plastics at those facilities and process them into flake or pellet grade, before shipping them into China. Because they are no longer classified as solid waste, the scrap restrictions don’t apply.

But the commodity codes that are used to identify products covered by the tariffs do not distinguish between resin made from recycled or virgin materials. Although an additional tariff on shipping certain pellets into China might not make or break a company’s decision to set up a new processing plant, it could dissuade companies from choosing to locate inside the U.S. while the tariffs are in effect.

“It depends on which grade they end up producing here in the U.S.,” Fu said. “If it happens to be the codes on the Chinese announcements, they will be subjected to the duty.”

Long-range concerns about materials and economy

Regardless of whether virgin plastics tariffs take hold and affect recycled values, producers of recycled plastic and some other materials could be impacted by the tariffs on aluminum that are already in place and causing market shifts.

Pickard, the ISRI economist, noted that companies that consume aluminum are currently being forced to pay more for the material than in the past. At this point, he said, that cost increase is being seen as a short-term bump that many are willing to withstand.

But if aluminum prices stay high for an extended period of time, companies that have typically used aluminum in packaging and products could begin to look for other options. Think more craft beer in glass bottles. Or more plastic pouches replacing aluminum cans for food products.

“The aluminum price might be higher short term, but if that reality is making aluminum a less competitive material long term, that could be worrying,” Pickard said.

That kind of shifting landscape on product and packaging material economics come as recycled paper and plastics are undergoing their own supply and demand uncertainties.

Jurden of Cook Paper noted that China’s scrap import restrictions have had a similar effect as tariffs – the policies have had a chilling effect on Chinese imports, they’ve disrupted the global flow of scrap commodities, and they’ve disrupted domestic and international prices.

“I think we’ve kind of endured the worst, but that’s a short-term perspective,” Jurden said. “Long term? That’s a great question.”

Ultimately, the unknowns surrounding the duration of tariff impacts are what seem to be spooking recycling executives the most.

“The question in my mind is what’s the definition of long term?” said Hawn of Machinex Technologies. “Right now you hear some people say we’ll be feeling the effects of this for 12 to 24 months. But then you hear other economists say it could be a lot worse.”

Many business organizations have come out hard against the tariffs, noting that historically, such measures lead to economic declines that can spread quickly across sectors.

“Tariffs imposed by the United States are nothing more than a tax increase on American consumers and businesses,” the U.S. Chamber of Commerce notes on its website, “including manufacturers, farmers, and technology companies, who will all pay more for commonly used products and materials.”

The Aluminum Association, meanwhile, has stated that aluminum import tariffs should be levied only on specific countries, rather than across the board. “The administration’s trade remedies should specifically target structural aluminum overcapacity in China, which is caused by rampant, illegal government subsidies in that country.”

Pickard said his group started having concerns as soon as tariffs were first mentioned at the highest levels of government, despite the fact the initial action has been a boost for many ISRI members.

His group has noted that taken holistically, the tariff action could “irreparably harm” the competitiveness of U.S. materials recovery stakeholders.

“In the short term, it has driven up prices along the ferrous supply chain, which is to the benefit of ferrous recyclers,” Pickard acknowledged. “But longer term, if that impacts pricing of materials that households have to pay, that’s going to put a break on personal consumption expenditures and economic growth. That’s bad for the economy and what’s bad for the economy is going to be bad for the recycling industry too.”

Dan Leif is the managing editor of Plastics Recycling Update and can be contacted at dan@resource-recycling.com. Colin Staub is the publication’s staff writer and can be contacted at colin@resource-recycling.com. Jared Paben, associate editor, also contributed reporting to this article.