This article originally appeared in the Fall 2018 issue of E-Scrap News. Subscribe today for access to all print content.

We all know electronics have become central to modern society, and disposal numbers quantify their growing ubiquity.

E-scrap volumes from U.S. households have increased from just over 200,000 metric tons annually in 1991 to a peak of 2.3 million metric tons in 2013, according to a study last year from the Rochester Institute of Technology.

A major component of that end-of-life electronics stream, of course, is plastics. In the period from 2003 to 2011, 25 U.S. states passed legislation related to the disposal of e-waste. And it’s estimated that those initiatives have made between 50,000 and 200,000 metric tons of e-plastics available for recycling each year.

For years, the bulk of the plastics stream moving through the U.S. electronics recycling infrastructure either went to China or was sent to disposal. Given the restrictions on the importation of scrap plastics to China and similar roadblocks being discussed in Southeast Asia, it’s no surprise that e-scrap recyclers, as well as major plastics and electronics stakeholders, are hungry for alternative approaches for handling these resins.

Can large scale domestic processing of this material emerge as a viable solution?

In this article, we’ll dig into that question, outlining the barriers that have prevented e-plastic operations in the U.S. up to now and presenting the details on strategies that would allow e-plastics to be recycled by domestic companies into high-value products suitable for sale directly to injection molders.

The key will be bringing enough investment and technical expertise into these endeavors to ensure the output meets market requirements.

Understanding specifics of the stream

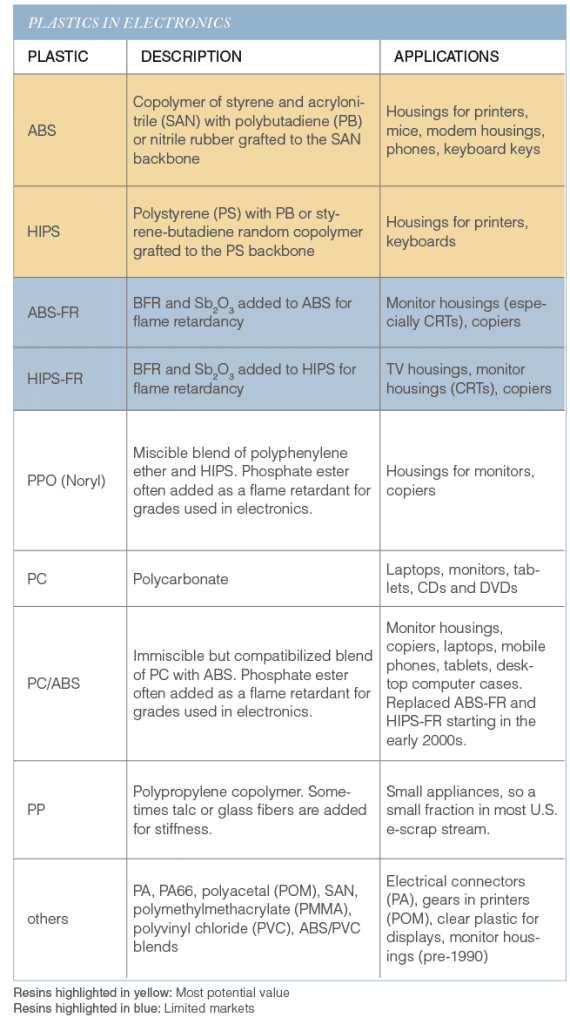

The electronics stream in the U.S. includes a wide variety of plastics, and a large portion of the polymers have significant value for recycling due to their good mechanical properties and potential for use in various new products.

These details are outlined in the table to the right. Plastics of most potential value for recovery are highlighted in tan. Plastics with limited markets due to the presence of halogens (especially brominated flame retardants, or BFRs) are highlighted in blue.

Indeed, it is the presence of halogens that so severely complicates e-plastics recycling. Let’s start by briefly describing why such engineered resins mark the stream.

Plastics in electronics in the U.S. must typically meet safety requirements and are often tested and listed with Underwriters Laboratories (UL). In products where a risk of fire exists (such as a plastic housing containing a source of high voltage or current), the plastics must be self-extinguishing with a UL 94V-0 or 5VA rating. Plastic parts without a risk of fire (most printer housings, keyboards and mice, for example) do not need to be self-extinguishing, so plastics with a UL 94HB rating can be used.

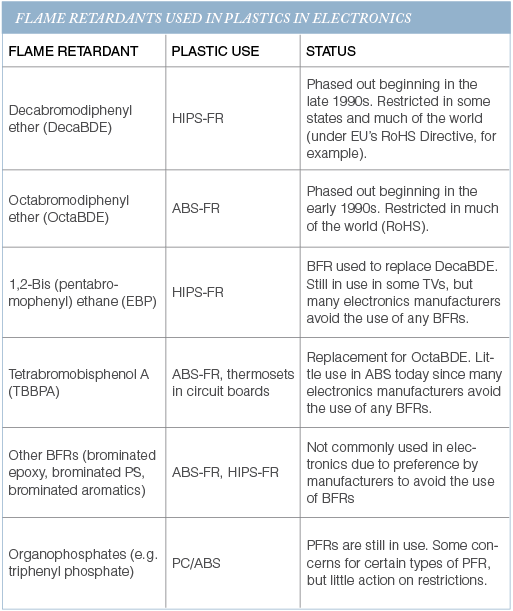

Flame retardants must be added to most plastics to achieve UL 94V-0 or 5VA ratings. For ABS and HIPS plastic resins, flame retardancy is typically achieved by adding a BFR at levels of approximately 12-15 weight percent along with antimony trioxide (Sb2O3) at levels of approximately 3-5 weight percent. For PC/ABS plastics, flame retardancy is typically achieved using phosphate ester flame retardants (PFR).

Housings for cathode-ray tube (CRT) monitors were often produced using either ABS-FR (for computer monitors) or HIPS-FR (for TVs), as these materials were relatively low cost compared with PC/ABS. However, concerns about certain types of BFRs (and halogens in general) began in the late 1990s and increased through the early 2000s. Many electronics manufacturers switched to “halogen-free” plastics (especially PC/ABS) in the mid-2000s at about the same time that CRTs were giving way to flat screen displays. For this reason, CRT plastics in the e-scrap stream today often contain BFRs, but fewer BFRs are found in plastic housings for flat screen displays.

The table below summarizes the types of flame retardants historically used in various plastics in electronic and electrical devices. Flame retardants that are restricted under the European RoHS Directive (and other analogous regulations in many countries as well as in some U.S. states) are listed first.

As noted above, BFR concerns have arisen due to possible health issues, the persistence of BFRs in the environment, and the formation of brominated dioxins and furans during poorly controlled combustion. Regulations have been implemented to restrict the use or disposal of several BFRs.

This means that to effectively recycle recovered e-plastics into new materials that can meet the requirements of manufacturers and regulatory bodies, the segment of the stream containing BFRs must be separated. This is no easy feat. While the types of plastics used in electronic applications is understood, the overall compositions of plastics in U.S. e-scrap is less clear, with little data publicly available. A study from 2000 (prepared by Headley Pratt Consulting for the American Plastics Council) gives the plastic composition for some U.S. e-scrap streams, but this data is outdated due to significant changes in product types and use of BFR plastics over the past two decades.

In short, further analysis and dissemination of information about the plastics found in e-scrap plastics would be of great value to recyclers considering further processing of these materials. Chinese processors had this information and could adapt quickly with their reliance on low-cost labor, but if more automated processes are installed in the U.S., it will be important to understand the composition in order to properly design processes and size equipment.

In short, further analysis and dissemination of information about the plastics found in e-scrap plastics would be of great value to recyclers considering further processing of these materials. Chinese processors had this information and could adapt quickly with their reliance on low-cost labor, but if more automated processes are installed in the U.S., it will be important to understand the composition in order to properly design processes and size equipment.

Key considerations for processors

Assuming the composition of plastics in the stream can be suitably understood, the next question is how to effectively separate the material during recycling. E-plastics may be recovered and recycled into high value products using a number of process steps.

The removal of most BFR-containing plastics could be accomplished by identifying products most likely to contain BFR plastics (notably CRT televisions) and segregating them prior to shredding. The remaining e-scrap could then be shredded and further processed using a variety of commercially available approaches to recover metals and other materials and to create a plastic-rich stream.

Once plastics have been segregated, the key is removing any remaining BFR plastics and to purify the various plastic types in the shredded mixture.

As many readers know, a number of methods may be employed to separate plastics from each other to create streams of purified plastic flakes. Plastics are often separated from each other based on density differences, though some plastics have similar densities so cannot be purified by such processes alone. Methods such as optical sorting and separations based on differences in triboelectric charging of plastics have also been used to separate plastic materials even when they have similar or overlapping densities.

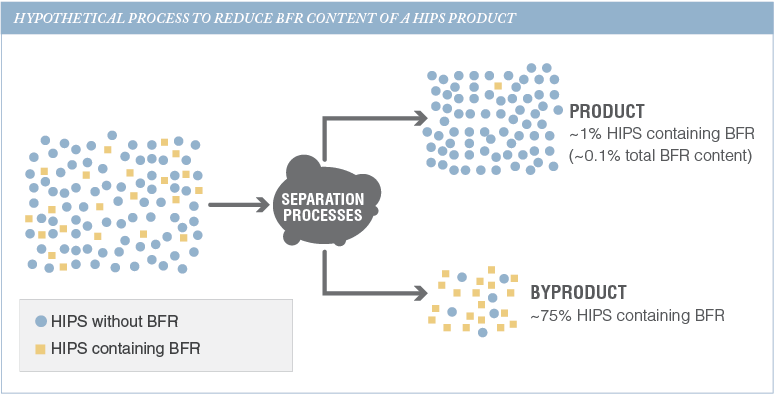

Some of the well-known methods used to separate plastics are also useful for reducing the content of BFRs in the final plastic products to acceptable levels (see figure below). Plastics such as ABS-FR and HIPS-FR typically contain BFRs at 12-15 percent by weight, whereas many manufacturers require BFR contents to be below around 0.1 percent to ensure compliance to the European RoHS Directive or to achieve “low halogen” limits.

It is important to note that more aggressive processing (either through tuning of process equipment or by processing through multiple separation steps) should be capable of reducing the BFR content to even lower levels, but such strategies naturally mean processing costs will increase. There is therefore a tradeoff of BFR levels versus cost (in addition to any regulatory limits) that a plastic recycler and its customers must consider when establishing specifications for recycled plastics from electronics.

Once reliable processing systems have been established, the focus of a recycler turns to customer relations. Buyers will expect the following from a supplier of recycled plastics:

Once reliable processing systems have been established, the focus of a recycler turns to customer relations. Buyers will expect the following from a supplier of recycled plastics:

- Plastic pellet material (or clean flake for compounding) that is free of contamination and meets certain properties.

- Technical data sheets (TDS), safety data sheets (SDS), certificates of analysis (COA) and declarations of post-consumer recycled (PCR) content and/or RoHS-compliance.

- UL listings for products to be used in electronic applications.

- ISO 9001 and ISO 14001 certification, to ensure that processes exist to ensure quality and to make quality improvements.

- Testing of incoming feed, intermediate products and final products for quality assurance.

- High quality technical support and troubleshooting capability.

Investigating the economics

As mentioned at the start of this article, the Chinese market has typically taken in much of the e-plastics recovered for recycling in the U.S. This trend was driven in part by low shipping rates (containers carrying goods to North America from China need to be sent back to Asia so carriers offer discounts for material going that direction). Other important factors included lower disposal costs of byproducts in China (or sale of byproducts into inappropriate applications), reduced processing costs in China based on lower labor costs, and large markets for a range of recovered plastics.

Apart from the fact that China has moved to severely limit imports of e-plastic material (and many other recyclables), we also now recognize that plastics containing BFRs should be disposed of in modern landfills or using advanced incineration technologies rather than being used in new products. That means that China’s exit from the e-plastic marketplace gives U.S. stakeholders the opportunity to handle this material in a more socially and environmentally aware manner.

And according to an economic analysis we’ve undertaken, the development of domestic processing can be highly profitable.

The analysis investigated how various factors would affect costs and revenues for a theoretical e-plastics recycling plant in the U.S. It includes the following assumptions:

- Annual supply of plastic to the plant is 15,000 metric tons.

- Plant throughput is approximately 3 tons per hour and plant operates in three shifts.

- Plastics from CRTs are not included in the feed.

- The mix of plastics in the feed is approximately 31 percent ABS or HIPS, 55 percent PC or PC/ABS, 9 percent ABS-FR or HIPS-FR (BFR plastics) and 5 percent other plastics (non-BFR). This is a rough approximation of the mix of non-CRT plastics in the e-scrap stream today, though further analysis would be required in order to verify this.

- The plant’s cost to acquire this mixed plastic feed is $0 per metric ton (delivered) since it would otherwise go to landfill or incineration due to the presence of BFR plastics in the mixture.

- Processed mixed plastics without any BFR plastics (but with some contaminants such as rubber and wood) can be sold for $150 per metric ton to other plastic recyclers/exporters or for downcycled applications.

- Sales price for purified flakes is between 30 and 50 percent of the price for the corresponding virgin plastics (for this analysis, prices published by Plastics News in June 2018 were used as the basis for value assessment).

- Sales price for pellets is between 50 and 70 percent of the price for the corresponding virgin plastics.

- Disposal of plastics containing BFRs is to landfill at a cost of $60 per metric ton.

- Yield efficiencies (actual yield divided by percent in feed) for product plastics are between 70 and 85 percent.

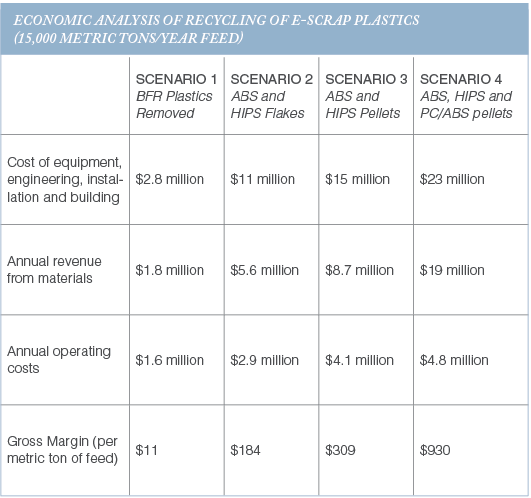

Using the above assumptions, we analyzed the financial realities of four operational scenarios.

In the first, the recycling plant only removes the BFR plastics to produce a mix of non-BFR plastics suitable for later recycling (including by export). In the second, the plant produces purified ABS and HIPS flakes that can be sold to compounders (companies that mix polymers and additives to achieve a market-ready blend). In Scenario 3, the plant produces ABS and HIPS pellets that can be sold directly to injection molders. And in the final scenario, the plant produces ABS, HIPS and PC/ABS pellets that can be sold directly to injection molders.

In each, we plugged in economic details related to the assumptions described earlier to determine a rough estimate of costs, revenue and gross profit margin for the facility. The findings are laid out in the table below.

The results clearly suggest that increasing amounts of processing will lead to greater gross margins compared with processing merely to remove BFR plastics or to create purified flakes for sale to compounders. We should note that the more advanced approaches of recycling into pellets do tend to require additional time to achieve the “steady state” economics in the model, as both the separation techniques and markets must be developed over time.

The results clearly suggest that increasing amounts of processing will lead to greater gross margins compared with processing merely to remove BFR plastics or to create purified flakes for sale to compounders. We should note that the more advanced approaches of recycling into pellets do tend to require additional time to achieve the “steady state” economics in the model, as both the separation techniques and markets must be developed over time.

Also, as all recycling veterans know well, the conditions around costs and downstream markets change often. With that in mind, the next step of the analysis was to look at how plant performance in each of the scenarios would shift if different economic factors underwent undulations.

The first variable we took into account was raw material cost. Our initial analysis assumed this cost to be zero, but what would happen if the plant instituted a tipping fee of $60 per metric ton or was forced to pay $100 per metric ton?

Another important variable is the price for virgin plastic pellets (used as a basis for all plastic feed and products). We looked at how the plant would be affected if prices were only 75 percent of our initial assumption as well as the impacts of virgin pellets increasing to 125 percent of our assumed value.

We also looked at what would happen if CRT monitors were included in the feed, meaning a larger portion of BFR plastics would be in the processing mix.

Finally, we considered the effects of excluding flat screen monitors from the feed so that there is a lower portion of PC and PC/ABS.

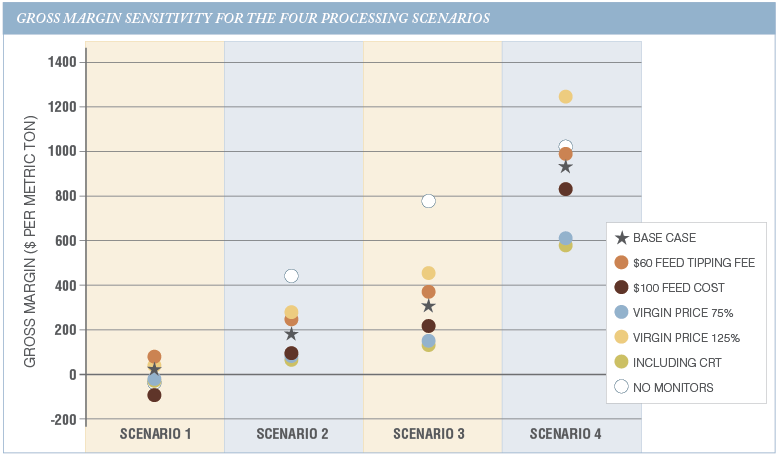

The results of these sensitivity analyses are summarized in the figure below, where the base values (black stars) are shown along with results for different values of the various parameters (while other parameters are fixed).

As that figure shows, the gross margins in Scenario 1 proved to be the most sensitive to the feed cost, with the highest positive gross margin in cases where a tipping fee is paid to the processor.

The mix of e-scrap products in the feed is most critical for Scenarios 2 through 4, though the price of virgin plastic is also of considerable importance. The highest gross margins are expected when all monitors (CRTs and flat screens) are removed, and the lowest gross margins are expected when CRT plastics are included in the feed. Higher virgin plastic prices are also helpful and can lead to the highest gross margins.

We also looked at the effect of feed volume on the economics and found that a factory with double the capacity (30,000 metric tons per year of feed) would be significantly more profitable (by between $30 and $60 per metric ton). We also found that factories operating in one or two shifts (compared with three-shift operations) are much less economically viable due to the longer return on investment as well as losses in efficiency. Efficiency losses are especially critical for the production of pellets, since considerable time is required to warm up extrusion equipment prior to start-up.

Trends that could reshape marketplace

There are a number of trends that should be considered as part of any serious study in the development of a business to recycle plastics from e-scrap.

The types of electronic products has and will continue to change over time, a fact that will naturally affect the plastics found in the e-plastic stream – there will be fewer BFR-containing plastics and larger amounts of plastics such as PC and PC/ABS. There’s also a possibility that products not often found in the current U.S. stream (such as small household appliances, which are a key component of European electronics recycling frameworks) could become part of the recovery mix.

Regulations around e-scrap could also shift and impact plastic recycling efforts. No new states have added e-scrap legislation since 2011, and the likelihood of legislation at the national level is low, but there will likely be small changes at the state level to ensure that any funding from the states (or from product manufacturers) adequately covers the costs of recycling. This could potentially help fuel investment in e-plastic processing.

Regulations regarding the use of post-consumer recycled (PCR) content plastics in new products may also become more prominent in the U.S. as there is a growing recognition of the value of recycling materials. This fact could be a driver for more e-plastic recovery, but potential regulations restricting the use of all BFRs in new products could limit outlets for some plastics recovered from electronics.

Potential changes to business models from the current approach to more “circular” service-based approaches focused on repair and reuse could also affect the types and amounts of products in e-scrap. More widespread repair and reuse would lengthen the lifetime of products before they are recycled, and fewer new products would be purchased, so there would be less end-of-life material in general.

A final trend we might expect in the coming years is further development of technologies to recycle e-plastics. There have been incremental improvements in plastic recycling technologies over the past decade, but with larger domestic markets, equipment manufacturers have a larger incentive to develop technologies to enable plastic recycling. While e-scrap plastic volumes are much smaller than streams such as packaging plastics, mechanical separation technologies developed for those streams should also improve the ability to recycle e-plastics. Solvent-based recycling technologies may also be further developed and implemented to improve the yields and quality of plastic products from e-scrap.

Next steps

Implementation of e-plastic recycling should begin with a feasibility study that includes the following steps:

- Characterize e-plastic streams.

- Determine potential volumes of e-plastics available (especially focusing on non-CRT plastics).

- Undertake a market study for outlets for recovered plastics.

- Develop a process flow for the e-plastic mixture.

- Estimate the capital and operating costs for the process.

- Estimate the economics for the recycling of e-plastics.

Once the above steps are taken and the economic model is deemed promising, the potential plastic recycler should investigate the actual performance of equipment selected for the process flow. This is a critical step that requires careful coordination and that can require a significant investment in time and money. Therefore, involvement by third- party experts can help ensure that appropriate tests are performed and that results are interpreted correctly.

Results from the performance tests can be further used as inputs to the economic model. These results can then be used to justify investment in the plastic recycling process, or may highlight areas requiring further study or business development.

Though it’s certainly true much work remains before these plastics are recycled into high-value products domestically, larger forces seem to be pushing the industry to take action on the e-plastic front. Exporting the plastics to Asia has proven to have economic and environmental risks, and that option is becoming increasingly challenging for U.S. stakeholders. A preliminary economic analysis demonstrates that recycling the plastics domestically can be feasible, though additional steps are recommended to verify the assumptions of the economic model.

Brian Riise and John Gysbers operate Sustainable Materials Recovery Group LLC (SuMaRec). Scott Farling runs Scott Farling Recycling and Materials Management. And John Dickenson represents Metamorphosis LLC. For more information about the research behind this article, contact briise@sumarec.com.