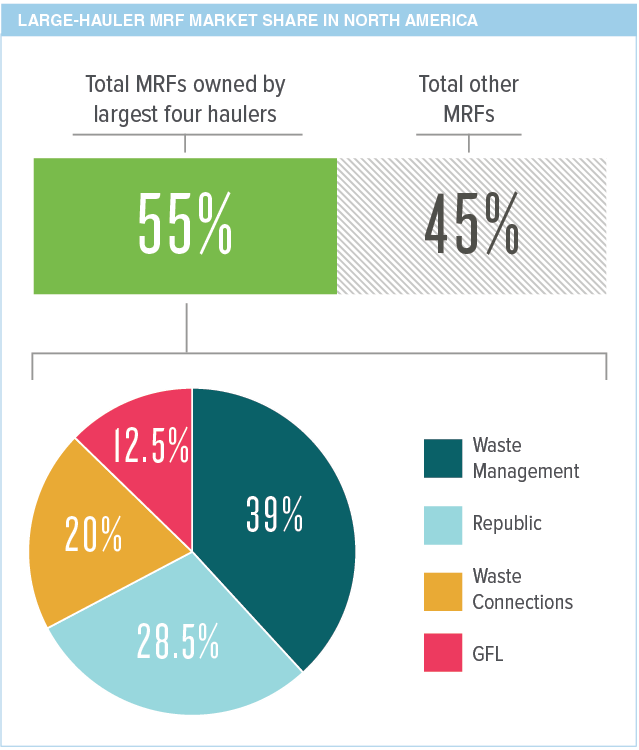

RRS analyzed MRF ownership in North America and found that over 50% of facilities are operated by one of four large waste companies: Waste Management, Republic Services, Waste Connections or GFL Environmental.

Recent acquisitions have underscored this long-running trend toward consolidation: Republic acquired ReCommunity; Waste Connections bought Superior and Progressive; GFL purchased Canada Fibers, Alpine and America Waste; and Waste Management added Advanced Disposal.

So is it a good thing to have the majority of MRFs run by just a few players?

On the pro side, the size of these companies creates more capital availability, which in turn enables greater investment in equipment and operations across an operator’s collection of facilities. Larger entities are also more resilient to market downturns because of their close integration with material buyers and other stakeholders.

Additionally, the economies of scale built into these companies can improve efficiencies in operation and promote lower accident rates because of more effective and comprehensive employee safety programs. Large waste firms also enjoy direct material sales to end markets with accrued monetary premiums in exchange for volume.

But there are downsides to a consolidated MRF ownership pool as well.

The natural objective of large firms is to maximize profitability, an economic good. However, this reality can conflict with local community values around materials management – for instance, residents’ wish to recycle more items. Also, the desire of the “bigs” to standardize equipment and processes across markets can reduce opportunities for motivated municipalities that may want to create customized solutions to maximize landfill diversion. And the waste giants may be driven to limit acceptable-materials lists to only those items that have the strongest markets at any given time.

Finally, limited competition in a regional processing market reduces vendor choice for municipalities, which could negatively affect contracts and rates – and weaken the motivation to innovate. These stresses tend to be heightened during down markets.

Today, larger companies provide a series of opportunities to breathe new life into struggling municipal programs, and they are indispensable to the wider system. They offer capital and influence that can be leveraged to improve recycling and develop local circular economies (though it’s important to remember they must get paid appropriately if they are to effectively utilize their size to perform the services demanded by the public). However, local, regional and public-private partnership efforts are also needed in the materials-processing ecosystem to provide disruption and avoid industry myopia.

This month’s Data Corner was produced by RRS. Learn more at recycle.com.

This article appeared in the March 2020 issue of Resource Recycling. Subscribe today for access to all print content.